Interview on France 24 TV channel

Christophe Alliot, president of BASIC, was interviewed on France 24 TV channel on Easter Sunday to discuss the environmental impacts of cocoa production and consumption and the potential for improvement.

Cocoa farmers produce around 5 million tonnes of cocoa beans each year. European Union consumes nearly half of this production in the form of chocolate, mostly during Easter and Christmas.

Interviewed on France 24 TV channel on April 20, 2025, Christophe Alliot, president of BASIC, talked about how the massive production of cocoa has an impact on deforestation and thus on climate change. He also explained what can be done to improve the situation both for the environment and for cocoa growers.

Watch it here:

Photo : Tetiana Bykovets / Unsplash.

It’s a little-known component used in many products: mica. This mineral has several interesting properties. Its glossy appearance enables it to be used in cosmetics such as nail polish and lipstick, but also in DIY paints. Its thermal and electrical insulation properties are prized in the construction of batteries for electric vehicles.

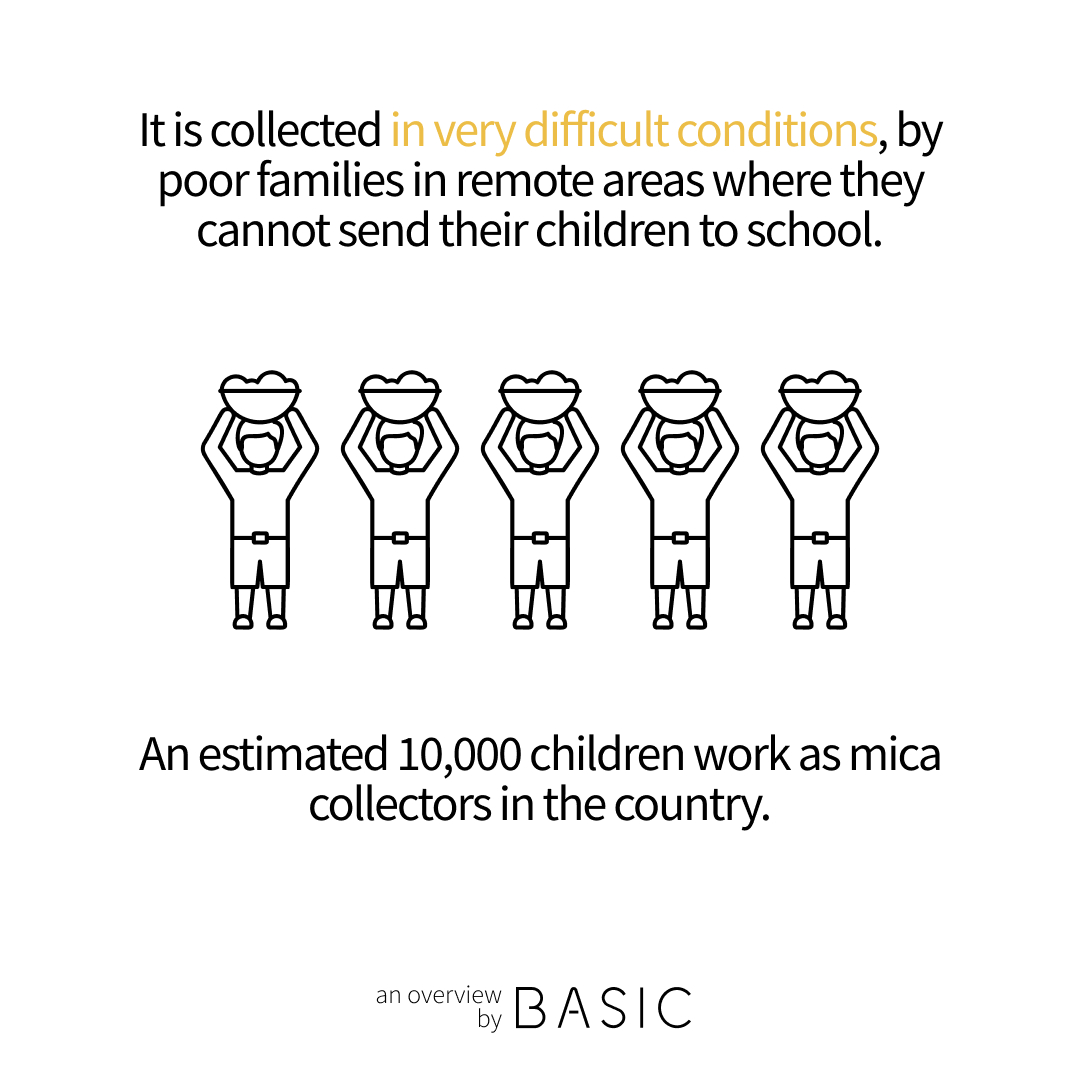

The problem lies in the conditions under which mica is collected. The people who extract or collect it earn extremely low incomes, which do not lift them out of poverty. The industry also makes extensive use of child labor, partly because mica extraction takes place in areas where there are few or no schools, and partly because families take their children with them to harvest the ore and slightly boost household incomes.

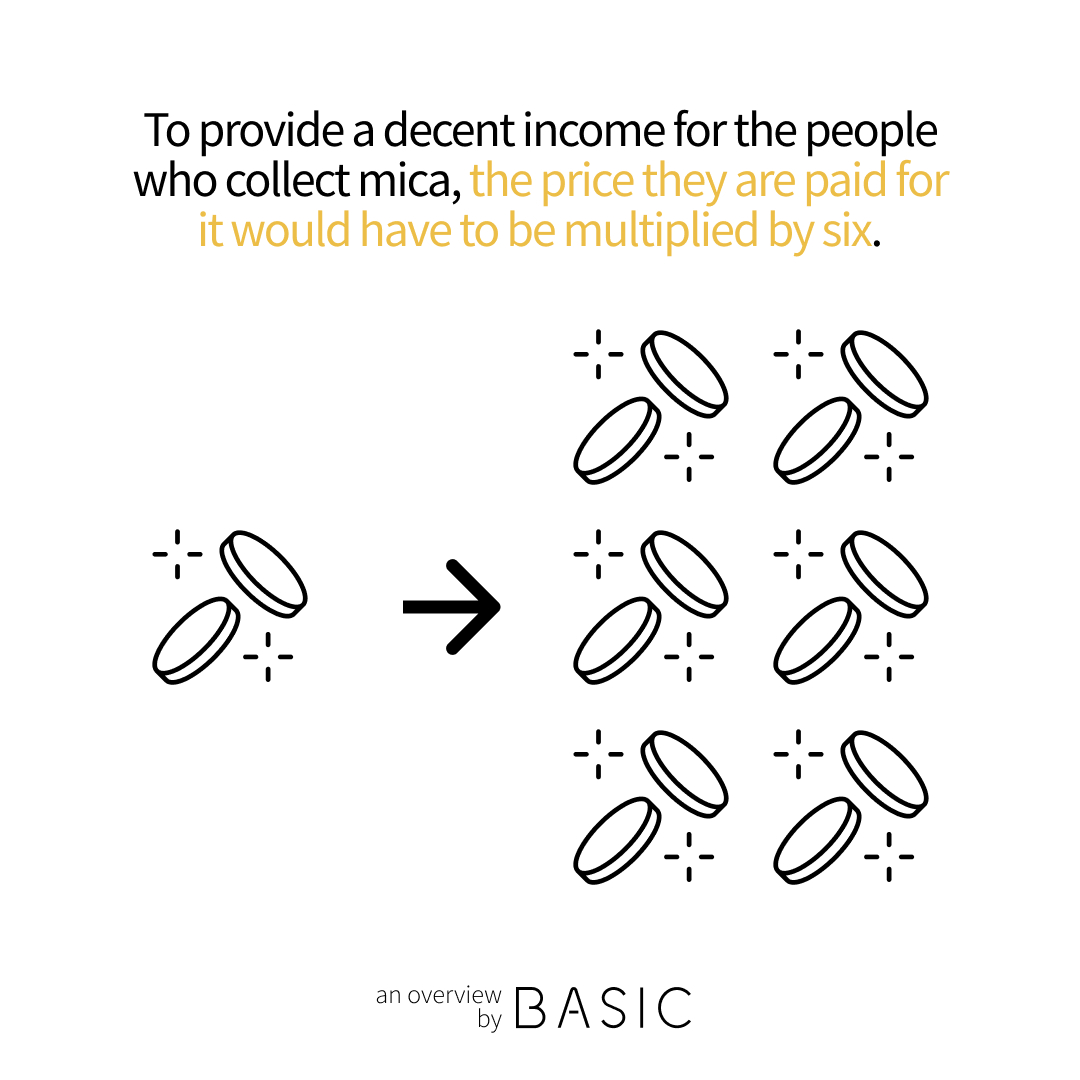

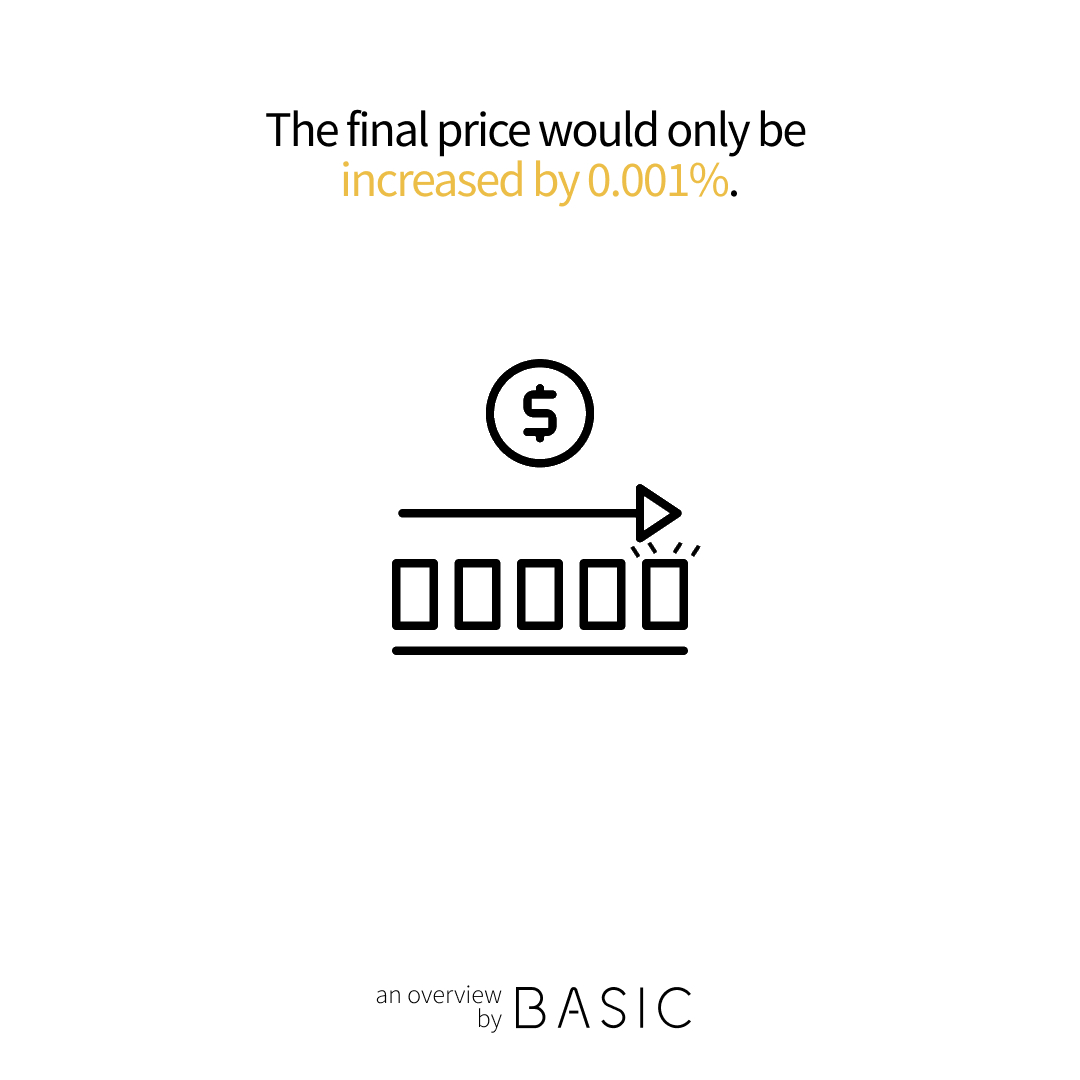

Guaranteeing a decent income for these families would lift them out of poverty and put an end to child labor. But what would be the cost for products containing mica? That’s what we set out to find out, at the request of the Responsible Mica Initiative. In 2023, we focused our research on mica mined in India. This time, we focused on mica from Madagascar, another major producing country. If the people who collect mica there are to make a decent living, the price they are paid for their mica would have to be multiplied by six. Looking just at the impact on batteries, vehicle insulation, and paint, this would only increase the final price of electric cars by 0.001%.

Photo: Michael Fousert / Unsplash.

Warning: Undefined array key 2 in /home/lebasic/www/v2/wp-includes/class-wp-query.php on line 3733

Warning: Undefined array key 3 in /home/lebasic/www/v2/wp-includes/class-wp-query.php on line 3733

Warning: Undefined array key 4 in /home/lebasic/www/v2/wp-includes/class-wp-query.php on line 3733

Warning: Undefined array key 5 in /home/lebasic/www/v2/wp-includes/class-wp-query.php on line 3733

Warning: Undefined array key 6 in /home/lebasic/www/v2/wp-includes/class-wp-query.php on line 3733

Warning: Undefined array key 7 in /home/lebasic/www/v2/wp-includes/class-wp-query.php on line 3733