Global value chains

Global value chains

When we study the links between the functioning and sustainability of a region or value chain, the first step is to analyze the metabolism of the area concerned. What are the flows of raw materials and products? Where do they come from? What volumes are produced? Who produces them? Where are goods sent? Who consumes them, and in what quantities? How do these orders of magnitude evolve over time?

These questions, and many others, are essential to understand the situation of a sector or region, its dependence on the outside world, and the level of connection between the various stages in the chain, from production to consumption, via processing and distribution.

To answer these questions, BASIC relies on a wide range of publicly available statistics (INSEE databases, ministry statistics, public agency figures, etc.) as well as paid-for data (retail sales details, for example). To be usable, this data requires a great deal of coordination, consistency and contextualization, as well as a good knowledge of the methods used to avoid misinterpretation.

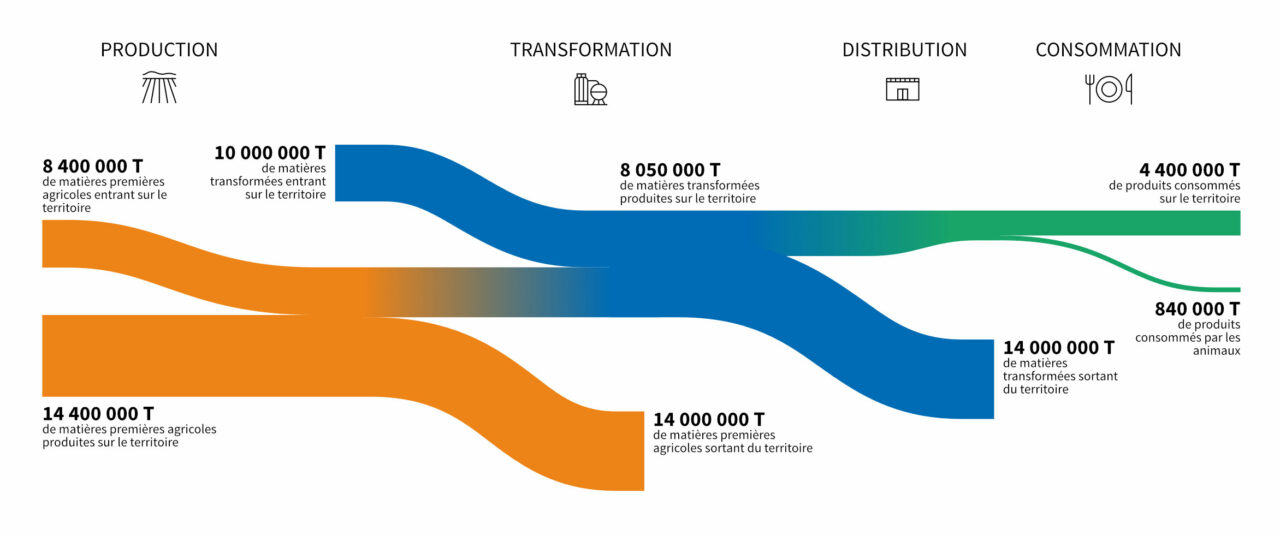

Source: BASIC modeling, 2019 based on SITRAM, SAA, PRODCOM, INCA, MAA, INSEE.

For example, these flow analyses enabled us to highlight Normandy’s role as a hub for cereals during a regional diagnosis: some of the cereals produced in the rest of France go through Normandy for export, taking advantage of the major port infrastructures of Rouen and Le Havre. However, the region is also a major importer of cereals, as the quality of those produced in the region does not always meet the requirements of the cereal-processing industries.

The flow analysis we carried out during our study of the French dairy industry showed that it was increasingly dependent on international trade. Imports have become essential to meet domestic consumption, while keeping prices low for foodservice operators and manufacturers who use milk-based ingredients in their processed products. Exports are also important for dairy manufacturers, who need outlets to make their factories profitable, as they engage in massive production aimed at reducing costs and increasing profitability.

Flow analysis also enables us to describe an essential phenomenon in the dairy industry: commoditization. Commoditization consists in homogenizing milk from farms and obtaining the most standardized characteristics possible, thanks to the blending of different supply flows. Using this process, the agri-food industry can rely on sources of raw materials that can be easily substituted for one another. This practice, which can be found in many agri-food sector, reduces the risk of variations in quality, and enables the industry to exert pressure on the prices paid to farmers. The mechanisms of price pressure, as well as its consequences in terms of economic gains or losses for the various value chain players involved, are the subject of the second part of our analytical framework.

Analysis of value creation and distribution

Rarely documented, the analysis of value creation, distribution and costs along a value chain is essential for an informed debate between its various stakeholders, whether it involves discussions on equity or anticipating the economic effects of new social or environmental regulations within an industry.

As part of our work on international commodity chains (cocoa, coffee, bananas, textiles, mica, etc.), or national ones (dairy, beef meat), we have developed our own method for analyzing the distribution of value and costs – as well as modeling and visualization tools – for consortia bringing together institutional and private players as well as civil society.

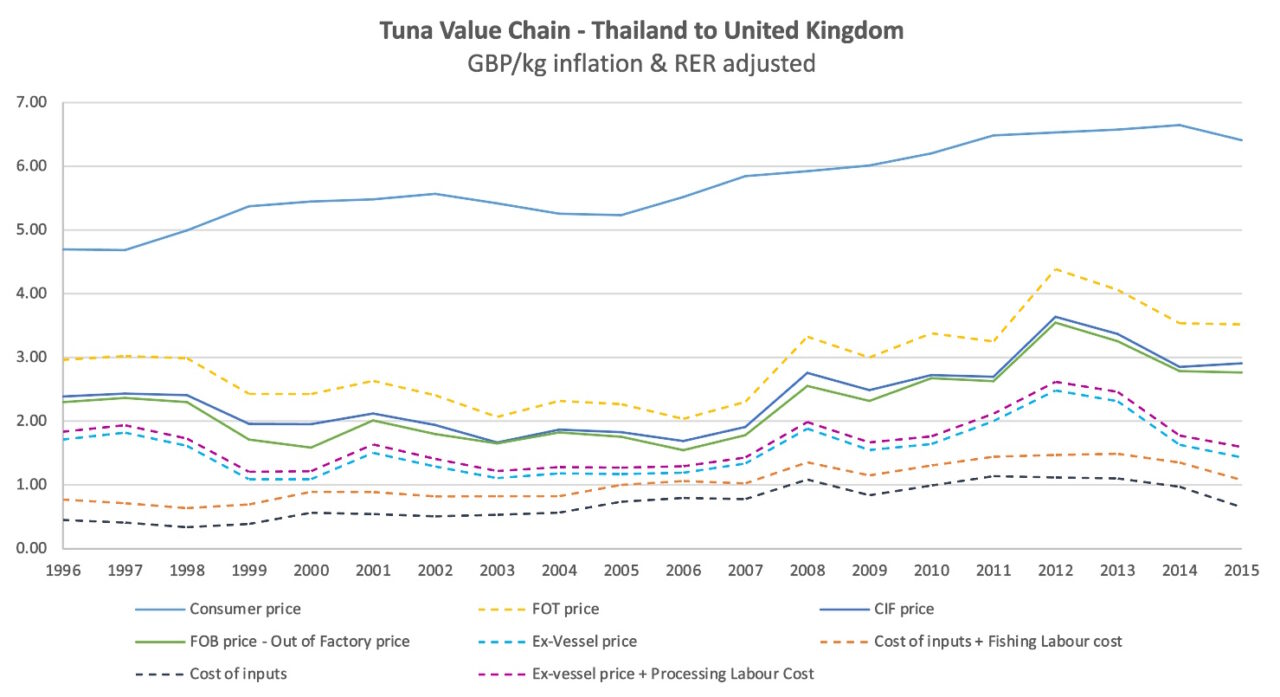

Part of our work on the creation and distribution of value involves analyzing price or cost levels at different stages in the chain, and their evolution over time. For example, one of our studies showed that retailers (led by supermarkets) capture the lion’s share of the selling price of tuna imported from Thailand to the UK. This share has risen sharply over the last few decades, from 34% in the years 1996-1998 to 45% in 2015. Over the same period, the share accruing to the fisheries fell from 20% to 6%. Faced with a rise in fuel costs and therefore in their operating costs, they have been unable to pass on this increase in the price at which they sell tuna to processors, due to their low bargaining power.

For work of this type, we have drawn on data from national statistical institutes, the UN Comtrade world trade database, academic studies and institutional reports.

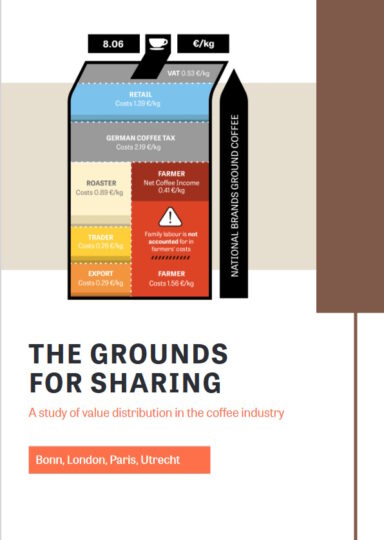

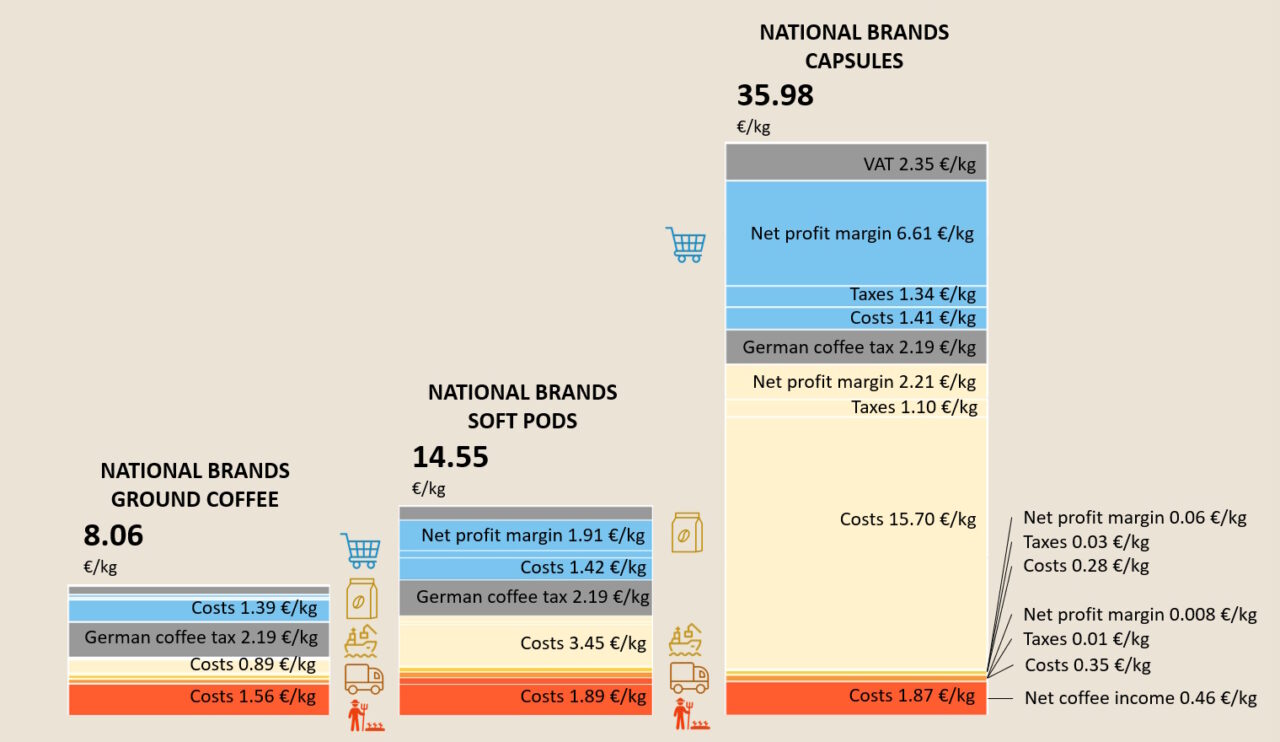

In other studies, we focus on a particular product – for example, coffee capsules – and refine the analysis until we obtain estimated costs, taxes and net profit margins of each stage in the chain. The cumulative net profit margin of collection, logistics, processing and distribution companies thus reached almost a quarter of the price paid by consumers for national brand coffee capsules in Germany in 2021. For ground coffee, the figure was just 4%. And yet, between these two types of products, the average income of coffee farms barely increased, rising from €0.41 per kilogram for ground coffee to €0.46 for capsules.

We carry out this type of study by consulting a wide range of data (some of which is available on a fee-paying basis), such as statistics from producing countries, company financial reports and sector-specific databases. We then model the market structure, the interactions between the various stages and the value chain. This work leads to an initial estimate of costs, taxes and net profit margins. At the same time, we conduct a large number of interviews with industry players to compare these estimates with reality, fine-tuning them and rectifying them if necessary.

Our studies on the creation and distribution of value can also focus on individual companies. For example, our work on the CAC 40 and SBF 120 companies has shown that between 2011 and 2021, the average pay gap between the CEOs of CAC 40 companies and the average salary within these structures rose from 93 to 163. Over the same decade, spending per employee in France’s 100 largest listed companies rose by 22%, while payouts to shareholders increased by 57%.

This work was carried out using the Orbis database and by compiling the information provided in each company’s reference documents.